A new client signs up on Monday and then by Friday, you’re still waiting on their proof of address.

The engagement letter went out on Tuesday – you think – but it’s somewhere in a thread between the client, your office manager and a junior who’s now on annual leave.

The AML check happened, you’re fairly sure (right?), but you’d need to dig through a shared drive to prove it.

If any of that feels familiar, you’re not running a bad practice, you’re running a fairly typical one.

How do we know? We have spent the last five years speaking with practices of every size and the themes are always the same, but within smaller firms the problem is more acute.

Most smaller UK accountancy firms onboard clients through a patchwork of email, PDF templates and well-meaning spreadsheets. Most are taught or assume that’s just how it has to be.

Of course, it isn’t – at least not with the advent of technology like Onboarder – and the cost of carrying on is higher than most firms realise.

Here are just some of the complaints we hear on a regular basis:

- Lost fee-earning hours

- Poor AML and KYC compliance

- Clients whose first impression of your firm is a list of documents and a slow response

Below are five signs your onboarding process is quietly costing you money and what a better setup looks like.

1. Senior staff are chasing documents

In most small firms, client onboarding starts well. A warm introductory call, a clear next step and then it all quietly stalls.

The proof of address doesn’t come back and the passport scan is in the wrong format or the client’s spouse is also a director and nobody asked for their ID.

The person who ends up fixing it is rarely the right one.

In firms with one to fifty staff, all too often partners and senior managers regularly step in to chase missing documents, clarify what’s needed or re-explain the AML process to a client who’s confused.

It’s not because they want to, but it’s because the process doesn’t have anywhere obvious for the work to live, so it escalates by default.

The cost adds up faster than you’d think. A senior manager on £65,000 costs the firm roughly £35 an hour fully loaded and that’s just their wage equivalent. In actual billable hours lost it could be far more.

Three hours of onboarding admin a week, across forty-six working weeks, is around £4,800 a year, per senior team member involved.

In a firm of ten, that’s easily £20,000 (probably more) of fee-earning capacity quietly absorbed by paperwork and chasing.

So, ask yourself the question:

In the last month, how often has a partner or senior manager personally followed up on a missing onboarding document?

If the answer is more than twice, then your existing process is leaning too heavily on the wrong people.

A better setup makes the onboarding stage self-driving.

2. The same client details get keyed in three times

Double or triple entry is the bane of every practice. It is time consuming and allows for too many errors to creep in from one platform to the next.

This can be a compounding issue when one-digit drifts or the wrong information is inputted across three systems.

However, if you have a starting point that everything is managed from during the client onboarding process, you create a single point of truth, which is then carried across all of your systems from the get-go.

This is also a great time saver, which can significantly reduce frustration in teams who are asked to do the same job three times, three different ways.

3. Your AML records would not survive an inspection

Every regulated firm has an Anti-Money Laundering policy and must run checks as part of the onboarding process. This is client onboarding 101.

The question your supervisory body is interested in is a much narrower one. Can you prove it, in the order it happened, against the risk you identified at the time?

ICAEW, ACCA and HMRC carry out AML inspections in broadly the same way. The inspector picks a sample of client files, often a mix of new and long-standing, and works through them to a defined checklist.

They want to see a documented firm-wide risk assessment, a documented client risk assessment for each engagement, evidence of customer due diligence proportionate to that risk, evidence of ongoing monitoring, and a clear audit trail showing when each step happened and who did it.

For higher-risk clients, they expect enhanced due diligence and a record of the senior approval that authorised the engagement

What they are checking, in other words, is not whether you have the right intentions. It is whether the file would stand up on its own if everyone who worked on it left the firm tomorrow.

This is where most small and mid-sized firms run into trouble, and almost always for the same reason. The work was done, but it lives in too many different places, creating an entirely fragmented audit trail.

From the inspector’s point of view, a control that cannot be evidenced is a control that did not happen.

The consequence ranges from a formal warning and remediation requirements, through to fines, and restrictions on the firm’s licence to act.

ICAEW publishes the outcomes of its disciplinary cases, and the underlying pattern in almost every AML matter is the same – not malicious failure, but the inability to evidence what was done.

Structured KYC and risk assessment records change that conversation entirely. With every client passing through the same documented flow, the firm-wide risk assessment feeding into each individual client risk assessment, the CDD and screening checks held against the engagement and a timestamped audit trail behind everything, an inspection moves from a defensive exercise to a confident one.

That shift is the practical difference between an AML programme that exists on paper and one that exists in the work.

4. Engagement letters take days to come back signed

The engagement letter sits in an awkward place in most firms. It is treated as an administrative formality and yet nothing else can start until it is back.

In a typical firm that posts engagement letters or sends them as a PDF attachment, signed turnaround is measured in days. Sometimes the better part of a week.

The letter sits in someone’s home office in a stack of post, or in an inbox alongside two hundred other unread emails, until a polite chase from the practice prompts the client to print it, sign it, scan it and send it back.

Even if you have an existing e-signing platform in use, it is often separate from the rest of your files or systems.

Templated engagement letters combined with e-signature change the picture immediately.

The letter is built from a standard template specific to the service line, populated with the client’s details from the onboarding record rather than retyped, sent through a recognised e-signature route, and signed from the client’s phone in the time it takes them to read it.

Typical turnaround moves from days, sometimes weeks, to hours.

That has two effects. The first is that work starts when it was meant to start, which is the answer to a great many capacity problems firms attribute to other causes.

The second is that revenue can be billed and recognised promptly, which is the answer to a great many cashflow problems firms attribute to client behaviour.

Neither effect is dramatic on a single engagement, but across a year of new client onboarding and annual re-engagements, the cumulative impact is significant.

5. New clients meet a clunky version of your firm first

A new client’s experience of an accountancy firm begins before any work is done.

The first interactions, be they ID requests, engagement letters, document uploads or initial information gathering, often set the tone for everything that follows.

By the time the first piece of substantive work lands on the partner’s desk, the client has already formed a view of how the firm operates.

Unfortunately, the world of accounting now has to face new perceptions of onboarding than in the past and clients will compare the experience to opening a current account through a banking app, instructing a solicitor on a property transaction, or signing up to a SaaS tool for their own business.

Many of these processes are now designed end-to-end, with any friction engineered out, so why shouldn’t they expect the same from their accountant?

Set against that benchmark, the traditional firm experience can feel jarring:

- Multiple emails requesting the same information in slightly different ways.

- PDF forms to print, complete by hand and scan back.

- Requests for ID copies sent over standard email with no clear indication of how the data will be held.

- Follow-up messages that arrive piecemeal over several days, each prompting a separate response from the client.

None of this looks bad in isolation, but in aggregate, it tells the new client that the firm runs on a chain of human prompts rather than a clear, codified system.

Whether the client articulates that thought consciously or not, it sits in the background of every subsequent interaction.

The interesting point is not that the technology to fix this is not exotic and readily available all within a single platform like Onboarder.

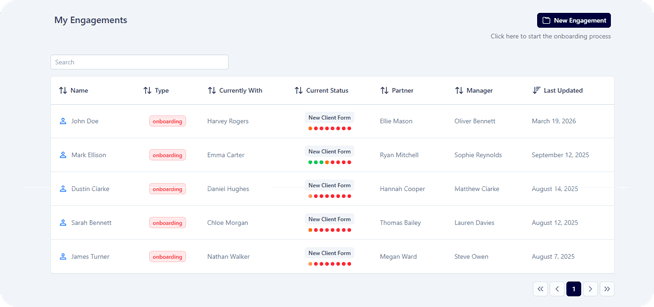

What better onboarding looks like in practice

Fit-for-purpose onboarding is a single end-to-end flow, not a collection of separate tasks jumbled together.

That is exactly what Onboarder is built to do.

As a cloud-based client onboarding platform designed specifically for accountancy practices, Onboarder pulls every stage of onboarding into one place, thereby cutting AML risk, accelerating engagement letters, removing the friction new clients feel in their first week and giving the firm a clean audit trail without anyone having to assemble it after the fact.

Crucially, it is configured around how your firm already works. Your service lines, risk methodology and engagement templates are all adaptable to your needs.

If any of the problems above sound familiar, Onboarder is the fix.

[Get started from just £20 per month]